Deep Dive Into Zomato

Zomato Limited has filed papers to go public in India, and is looking to raise $1 Bn. IPO Pricing is yet to be finalized.

This edition delves into Zomato’s business, and offers some thoughts on the India opportunity and valuation.

This edition is laid out in 5 sections

1. Business

2. Unit Economics

3. Zomato Mental Model

4. Valuation

5. Interesting footnotes

Usual disclaimers apply. This piece is for informational purposes only, and reader attention is urged at exercising their independent judgment. Nothing mentioned here should be construed as investment advice. The author may have ongoing interest in some, or all, the companies mentioned in this edition.

[I] Business

Incorporated in 2010, Zomato Limited is a premier Indian Food Services platform. In 11 years, it has managed to build a 3-sided marketplace connecting Customers, Restaurants and Logistics.

Zomato has two core B2C modules: 1) Food Delivery, 2) Dining out; and a B2B offering — Hyperpure. Finally, it also has a customer loyalty program (Zomato Pro) that combines (1) and (2). As of December 31, 2020, Zomato was present in 526 cities in India.

The Food Delivery business has three key stakeholders:

- Customers (5.8 MM Monthly Transacting Users as of Dec’20).

- Restaurants (131,233 Active Food Delivery Restaurants every month in fiscal 2020. 350,174 Active Restaurant Listings as of Dec’20).

- Delivery (161,637 Active Delivery Partners during the month of Dec’20).

The other monetization streams are:

Dining Out: Where customers use Zomato for Search and Discovery. This is presently monetized through advertisement sales from Restaurants listed on the platform. In fiscal 2020, 8,064 restaurants paid for this product.

Hyperpure (B2B supplies): This is the farm-to-fork supplies offering for Restaurants in India. Rolled out in 2019, Zomato has served over 6,000 Restaurants across 6 cities in India.

Zomato Pro: Exclusive loyalty paid membership program. As of Dec’20, Zomato had 1.4 MM Pro members and 25,350 Restaurant partners in India.

How does Zomato make money in Food Delivery?

Difficulty in building a 3-sided marketplace in India

The capital-light nature of running the business is visible straightaway. Zomato owns neither Restaurants nor the Delivery infrastructure. This keeps fixed assets low (1% of balance sheet). By virtue of its vantage point as a Marketplace connecting the 3-sided network, Zomato is the funnel of money flow in the system. This translates into modest working capital commitments (negative working capital for Zomato).

However, building the 3-sided marketplace is an extremely capital intensive endeavor. Restaurants and Delivery partners need to be induced to participate in the platform. To build this Supply, Demand (Customers) needs suitable inducements as well. As the unit economics illustrate, these inducements are a drag on Contribution Profit.

History offers interesting pointers into the difficulty in building such marketplaces in a country like India.

Over its 11-year history, Zomato has cumulatively raised around $1.6 Bn in external capital. Against this, it has achieved Revenues of $366 MM (full year 2020, as 2021 was a COVID distorted year); on an employee base of 3,469. Zomato is yet to turn a profit, however, as it has been in this capital intensive build-out mode.

For comparison, recently listed Deliveroo Holdings PLC (ROO; Market Cap = $6.5 Bn) is 7 years old. Deliveroo raised $1.5 Bn in external capital before its IPO. This helped it achieve Revenues of $1.6 Bn and is on its way to turning profitable. Deliveroo achieved this on a total employee base of 2,060. It listed at a $10 Bn market cap, but sold off as investors frowned at its dual share class structure, and as interest waned towards gig economy businesses.

The difference in capital efficiency trajectories in the two geographies is stark.

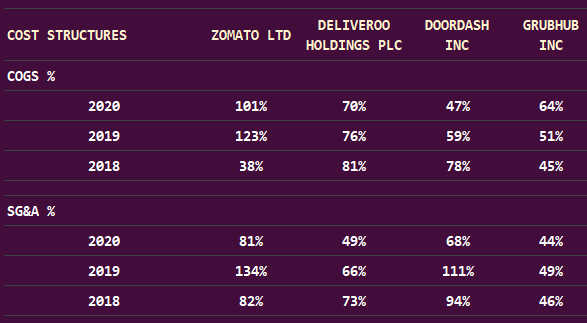

A closer look at the structure of the employee bases at a selection of food delivery-focused companies globally highlights the nature of the India market.

Zomato’s employee base is dominated by the Sales & Marketing function, which is a contrast to Deliveroo. The employee revenue efficiency is indicative of the boots-on-the-ground nature of building a business in India; even for a Technology-first business.

Food Delivery marketplaces are a hypergrowth, profitless business at the moment. However, scale helps some operating leverage to kick in, as seen from the cost structure evolution below.

The capital requirement to build scale in India acts as an entry barrier, warding off potential competition. The demands of Category Creation manifest in heavy capital expenditures, which tend to show up as Sales & Marketing spends. Most Indian start-ups tend to exercise this lever as a means of achieving scale; frequently at sub-optimal near-term unit economics. Average Transaction Value also tends to be lower in India than in Western geographies. This weighs on fulfillment costs and operating leverage. Many businesses that start out as Technology-first businesses find their future avatars calling for increasing boots-on-the-ground presence.

Whether scale in India can offset inferior capital efficiency over the long-run is a key question.

[II] Unit Economics

At a unit economics level, Zomato needs to deliver the following:

- Acquire Customers (‘Acquisition CAC’, or Customer Acquisition Cost). Hopefully, cheaply.

- Get them to Transact. The more the merrier (‘Transaction Volume’).

- Extract an Order Value per Transaction. Hopefully, increase this with time.

- Retain Customers (or, ‘Retention CAC’). Hopefully, cheaply.

- Extract a meaningful Margin.

- Repeat 1–5.

The IPO Prospectus mentions a lot but the variables crucial for contemplating future value creation find little mention in the 420-page document. So we resort to my favorite Fermi technique to guesstimate the essentials, as we dive deeper into the business labyrinth.

Many start-up decks tend to highlight LTV based on Revenue alone. It is more prudent to look at LTV based on retained Profit Margin, since fulfillment costs on revenue will determine future capital requirements through the cash flow lever.

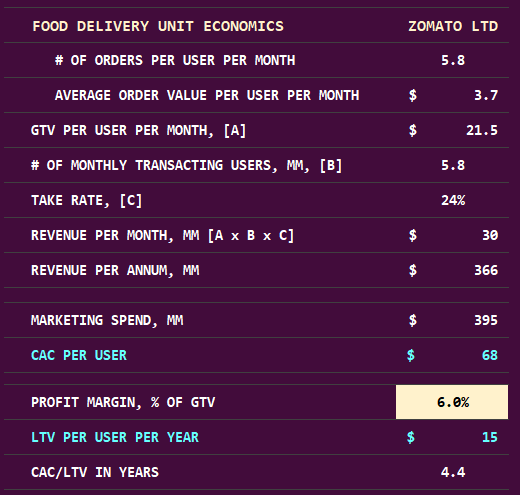

While Zomato shares Cohort behaviour on Ordering Value (more below), it does not shed much light on User Retention Cohort behavior — a crucial variable influencing long-run outcomes. The Unit Economics model helps triangulate how long an average User needs to continue as a paying customer for Zomato. The Unit Economics model makes an allowance for enhanced Profit Margin % on GTV (Gross Transaction Value). It assumes that Zomato (which is not profitable currently) will be able to extract an attractive 25% margin on its Revenue (GTV x Take-Rate).

One way to think of CAC is to look at Marketing spends and how much that has helped User creation. Zomato spent $395 MM in Marketing spend cumulatively over the past few years. This spend has helped it achieve Monthly Transacting Users of nearly 6 MM. This gives an approximate CAC of $68 per Transacting User.

The Unit Economics model indicates that Zomato needs a User to stick around for over 4 years on average before CAC pays itself back through profits. User Retention, or Churn, is one of the most crucial long-term variables in this business.

Backing out Unit Economics in rapidly growing businesses is an exercise in uncertainty: as fresh spends are needed to not only grow the user base, but also retain existing ones. The above estimation exercise points to the difficulty in monetizing the average Indian User. It also points to the demands placed on extracting a meaningful Margin at some point in the lifecycle.

More on Zomato’s Throughput variables

One of the ways for Zomato to drive revenue is to increase GTV with time. From its disclosures, it seems to be well placed on this front.

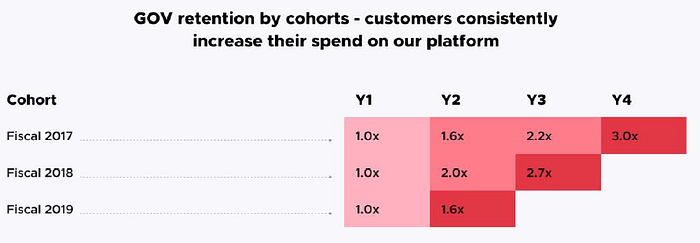

This GTV (or Gross Order Value GOV, in Zomato’s parlance) Cohort chart shows that Users step up Transaction spends over the years. Average Order Value has been rising through 2021 as well. A good outcome.

However, a second key variable that is needed to complete this picture is the User Retention Cohort — the proportion of Users that continue as Customers over time. Zomato tantalizingly makes a reference but no User Retention Cohort is forthcoming (there is zero mention of ‘churn’ in the prospectus).

The User Retention Cohort is crucial for CAC and LTV economics. Another reason why this metric is crucial is visible from the filings.

Stay-at-home lockdowns for most of 2020 should have boosted Zomato’s Transacting Users. But the metric went the other way.

In the absence of a User Retention Cohort, the volatile variable — Churn — can make, or break, long-term unit economics. Unless Zomato can find ways to offset this. The non-Food Delivery business offerings may help reduce this payback period over time. Another potential avenue is to extend the Hyperpure business to the Grocery vertical.

[III] Zomato Mental Model

Zomato’s market opportunity can be triangulated in several ways. One long-term hypothesis is to think about the proportion of home food consumption that will shift to Outdoor (or off-premise) Ordering.

Mental Model for Zomato’s India opportunity over the next decade:

- 3 meals a day x 7 days a week = 21 total meals per person per week.

- Shift: Assume 15% of total meals shift from home-cooked food to Outdoor Ordering mode, this will translate into an opportunity of 3.1 meals per person per week. Further, assume that 10% of India’s population shifts to Outdoor Ordering (i.e. 140 MM people).

- Spend: Assume ₹350/meal average spend per transaction. This represents India transaction TAM (Total Addressable Market) of $100–110 Bn p.a.

- Share: Assume Zomato manages a 35% market share, this will translate into $35–40 Bn of annual GTV opportunity for Zomato. This assumption (optimistic) allows for Zomato’s leading market position to strengthen over time, helping it sustain a dominant market position.

- Take Rate: Assume 20% revenue take-rate (optimistic, over a decade), this represents a $7–8 Bn potential Revenue pool of opportunity for Zomato in a decade. Translating into an eye-popping 35% Revenue CAGR over the next decade.

Indians have traditionally preferred home-cooked food. This behaviour has been changing in recent years for a variety of reasons, driven by demographic and lifestyle transitions. It is conceivable that the trend of more outdoor food consumption will increase with time. For comparison, in the US, food consumed off-premise was 50% of total Food & Beverage spend in 2019 (source: DoorDash).

India Food/Grocery Services is a competitive market with players such as Swiggy, cloud kitchen players, and grocery/consumables delivery players. M&A is another route that Zomato is likely to use to protect and grow into the assumed significant market share in a decade.

[IV] Valuation

Yours truly is a fan of very long-term outcomes.

What will it take for Zomato to deliver $7.5 Bn revenue in a decade?

In the coming decade, non-Food Delivery streams will likely start monetizing as well. But given the nascent stages of evolution today, we will assume that Food Delivery (or Grocery, which is an inevitable adjacent vertical) will be the primary driver of revenue.

To achieve this revenue, Zomato will have to:

- Increase Order Count by 2x to 12 Orders per user per month. This roughly translates to 3 orders per week; in consonance with (2) in the Mental Model above.

- Average Transaction Value to $5 (~₹350). These will combine to drive 11% CAGR in GTV over a decade.

- Assume Take-Rate stabilizes at 20%. Zomato will need to grow its Transacting User base to a little over 50 MM, or 9x from current levels.

Zomato’s IPO Pricing is yet to be announced. The last round of funding valued Zomato at $5.4 Bn. Some sources privately speculate that its listing valuation will likely be ~ $7 Bn. This outcome would necessitate 40% Revenue CAGR over a decade for Zomato and profit margins in the 20s. For contrast, other Food Service marketplaces of interest to us embed 20–25% Revenue CAGR and mid-teen profit profiles.

Zomato will have to grow at a stupendous rate, while retaining users, and extracting above-average economics; over a decade.

It has its task cut out.

A look at our fair value distribution for Zomato’s valuation.

In the short-term though, Indian markets are likely to evince strong interest in the offering. Along with its significant shareholder Info Edge (who will have an outstanding outcome on its investment), Zomato represents a tiny sliver of Internet Consumer Technology businesses that will be listed in India. Momentum is likely to be the dominant sentiment driver in the short-term, with operating realities falling at the sword of near-term euphoria.

[V] Interesting Footnotes

Some interesting footnotes from the prospectus.

Lock-up post offer

Foodiebay Employees ESOP Trust (ESOP 2014) holds 4.17% of pre-offer Equity share capital.

Overseas investments

The preamble to this footnote mentions ‘details of investment eliminated…’ but the header item reads ‘Provision for diminution in value of equity’. Zomato Limited had 36 active subsidiaries/step down subsidiaries/JVs, accounting for 15% of revenue in 2020. But overseas geographies will no longer be a focus area.

Over to the listing.